19/04: The Liquid Restaking Era

19/04: The Liquid Restaking Era

Latest LAVs and Exploring a Liquid Restaking Omnipool!

In this transmission, we look at the latest liquidity allocation votes (LAVs) results and the potential upcoming Liquid Restaking Omnipools.

Latest LAV results

The latest LAV went live on April 11th and concluded on April 16th. The newest distribution of each of the pools is as follows:

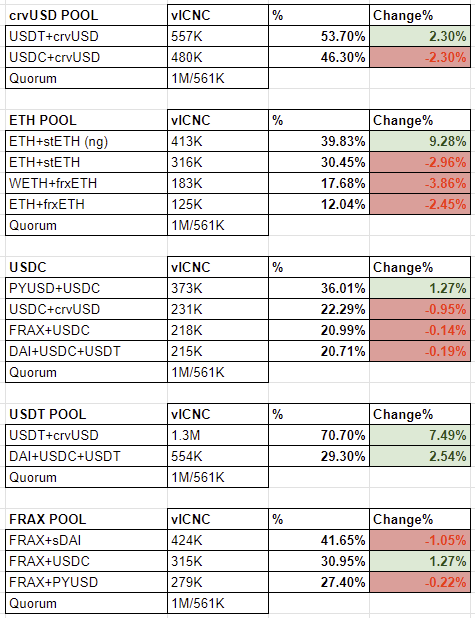

crvUSD POOL

USDT+crvUSD — 53.70%USDC+crvUSD — 46.30%

ETH POOL

ETH+stETH (ng) — 39.83%ETH+stETH — 30.45%WETH+frxETH — 17.68%ETH+frxETH — 12.04%

USDC POOL

PYUSD+USDC — 36.01%USDC+crvUSD — 22.29%FRAX+USDC — 20.99%DAI+USDC+USDT — 20.71%

USDT POOL

USDT+crvUSD — 66.76%DAI+USDC+USDT — 33.24%

FRAX POOL

FRAX+sDAI — 41.65%FRAX+USDC — 30.95%FRAX+PYUSD — 27.40%

The biggest gainer of these most recent LAVS is the ETH+stETH (ng) curve pool, which saw a 928 bps increase. Obviously, this meant a complete shuffle across the board within the ETH Omnipool with each of the other three pools losing a minimum of 245bps. WETH+frxETH took the biggest hit, dropping 3.86% of it’s Omnipool share.

The other biggest gainer that dominated the votes within the USDT Omnipool was USDT+crvUSD, which netted 749bps, up from 63.21% in the previous vote.

The Liquid Restaking Omnipool

We wanted to take a bit of time to explain how a Restaking Omnipool could fit into the current Liquid Restaking Landscape:

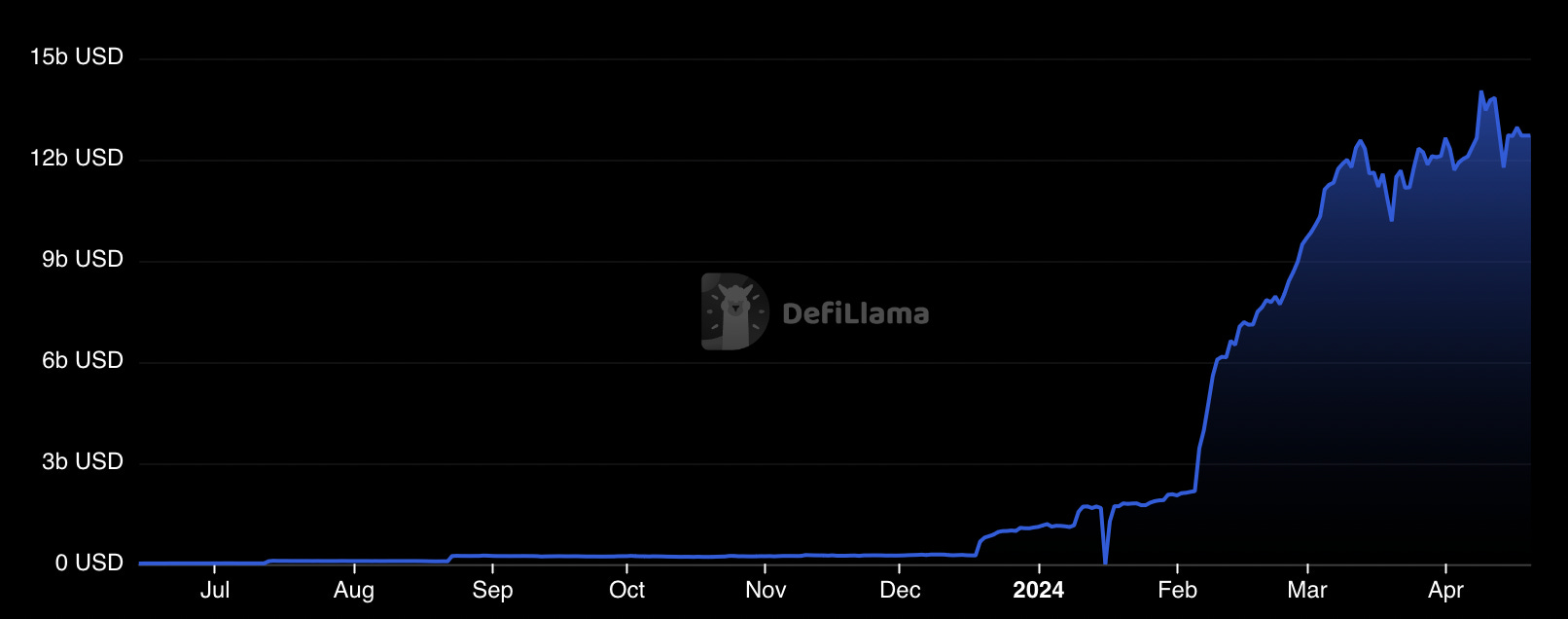

Since EigenLayer (EL) launched back in late 2023, it’s grown to amass over 4,711,123 ETH ($14,501,495,732) Total Value Locked (TVL). This massive amount of capital is a mix of native ETH and several Liquid Restaking Tokens.

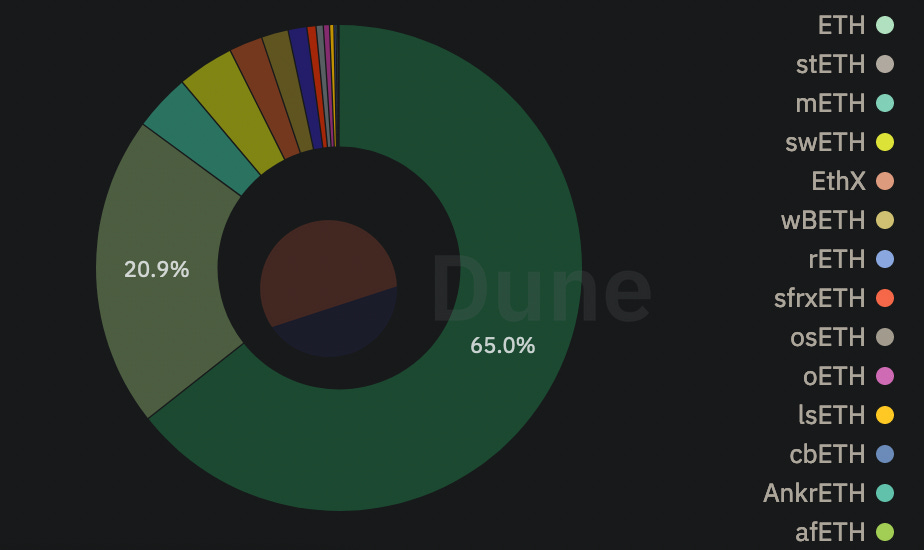

Native ETH is the most dominant, with 65% of the total restaked. Then there is Liquid Restaking tokens, which according to defillama, make up $9.517b of assets (potentially some double counting).

That is a lot of derivative ETH—most of these new protocols have taken deposits in stETH, rETH, and cbETH exchanged for their new liquid restaking tokens.

A significant portion of this capital deployed into these protocols has been used to farm airdrop points, which is a potentially additional yield on top of the yield-bearing derivative ETH token.

What’s interesting here, though, is that several of these protocols are not even live on the mainnet yet, so withdrawals aren't enabled. Most of them haven’t airdropped a token yet—but what happens when withdrawals are enabled, and airdrops have taken place?

One possible and likely scenario here is capital flight, which comes with one inherent risk that we will focus on as they are most relevant to Conic.

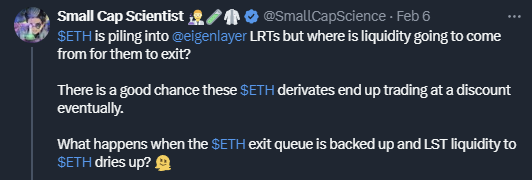

As highlighted here by Small Cap Scientist, LRTs have piled into EigenLayer, but exiting could be significantly more challenging.

Although these tokens can be withdrawn or will be able to be withdrawn when each LRT protocol enables withdrawals, exit queues could be significant. Therefore, capital will likely get trapped, and users who want a near-instant exit will have to look for liquidity in the market. Herein lies the problem.

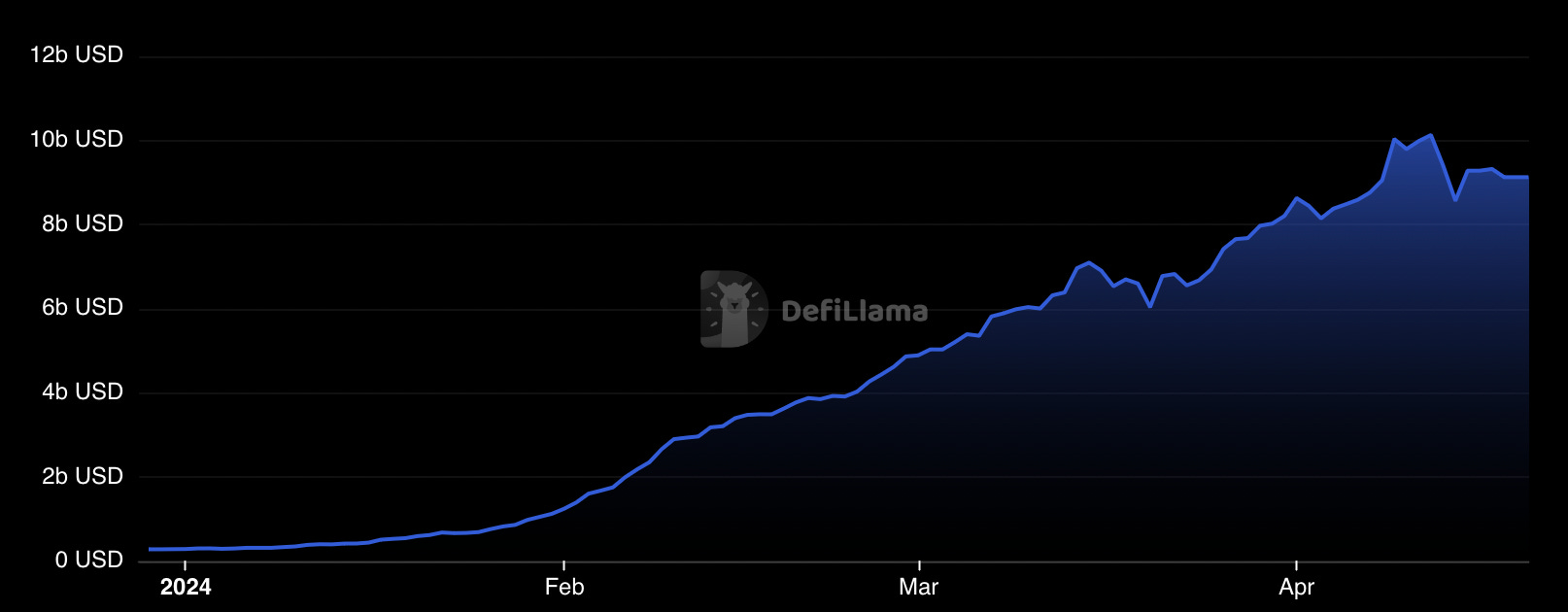

Now, it’s worth noting that this tweet thread was from early February, and the $800M TVL mentioned has grown to nearly $3.6B.

Coingecko shows weETH's market cap at $2.32B, with only 2.45% of that in liquidity ($57.24M). Now, $57M might seem like a lot if you’re only exiting with small amounts, but if any large entity chooses to use this pool, it could easily lead to a de-pegging event. Ether_fi’s eETH is the largest LRT, but many others have less liquidity.

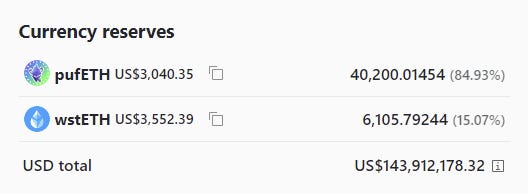

Another example is Puffer Finance, the second-largest LRT protocol ($1.237B in TVL), currently preparing for its mainnet launch.

Their PufETH/wstETH curve pool currently has $143M in liquidity, only 15.07% of which is in wstETH.

Other wstETH pools have launched or are launching on Curve, so it seems to be the likeliest candidate for a potential restaking Omnipool. Conic could become the pillar of vital liquidity direction for the many LRT protocols. Helping to ease liquidity constraint pains of all these protocols.

What would be this Omnipool’s draw be for liquidity providers? Well, it would receive the same yields from the Curve Pool and CNC (as per existing Omnipools) and potentially accrue airdrop points or incentives as a sweetener.

The above will undoubtedly require business development, and we know the team has been exploring this angle. It’s always exciting to speculate and discuss ways Conic could fill a vital niche, especially with how popular a narrative Restaking and its Ecosystem has become.

Either way, we’re both excited and interested to see which direction the team takes.

Awesome analysis. Agree LRT depegs are likely if withdrawal queues are not properly managed.