09/02: Post Launch Extravaganza

Conic Returns with a bang, amassing 30M+ TVL in just over a week!

In this latest transmission, we look at the V2 Launch, MixBytes Audit, the implementation of vICNC Bonding, the subsequent APR Rewards, and Conic’s post-launch growth!

The Launch

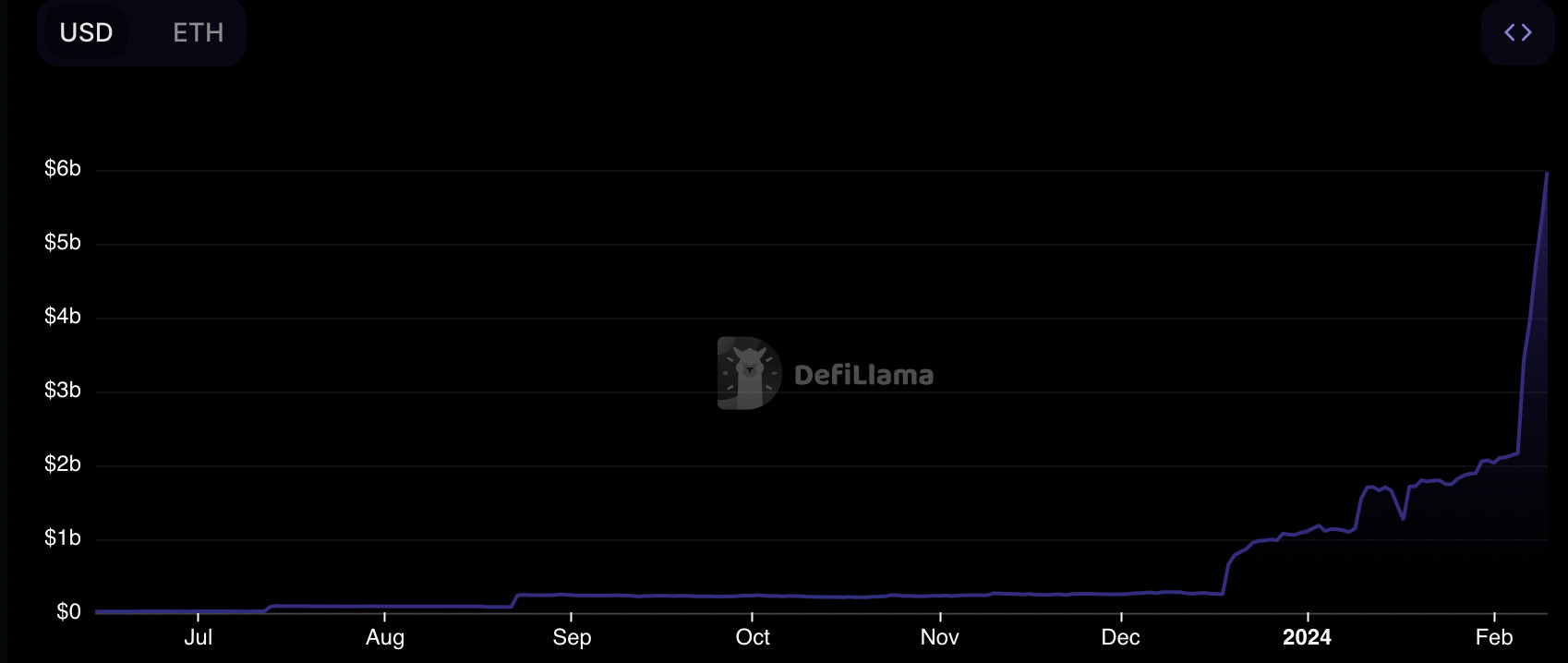

It’s here! V2 dropped on January 31st—a great way to close out the first month of the new year—as a highly anticipated launch for the Coneheads and the wider Curve ecosystem. We saw a crescendo of TVL deposited into the new pools, $20M within the first 24 hours.

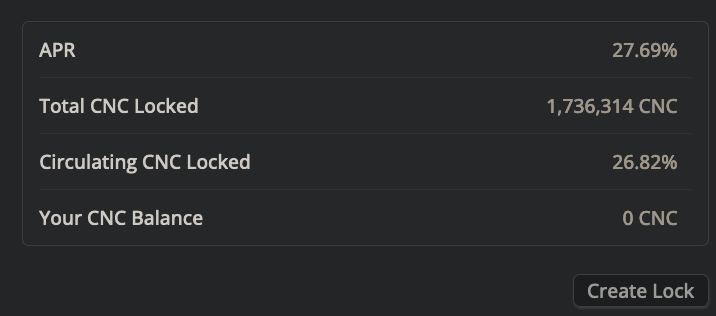

There has also been a spike in locked CNC, currently sitting around 26%+ in the last week, mostly due to the addition of vICNC APR rewards—but more on this shortly.

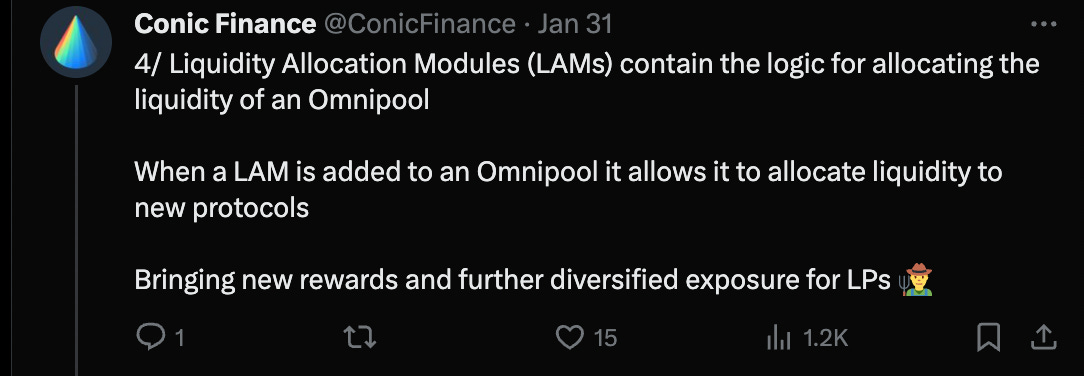

So what does Conic v2 introduce? Improvements, lots of improvements and a ton of new features. The most exciting is the introduction of Liquidity Allocation Modules (LAMs), which allow for modular liquidity provision across different protocols, expanding the rewards and exposure for liquidity providers (LPs).

If you’ve not heard of the term ‘modular’ in recent months, you’re definitely out of the loop—not just another buzzword, most new protocols (rollups, layer 2s, etc.) are being built with this modular design in mind—separate, interchangeable components that can be developed and deployed independently, allowing for flexibility, scalability, and easier maintenance.

How does that work with LAMs? Well, these new liquidity modules enable flexible liquidity allocation, which can be deployed into different protocols—customization is the main draw. Liquidity providers can choose assets to allocate into protocols customized around risk tolerance and market conditions, unrestricted by a single protocol. This enables easier integration with new protocols and adaptability with existing ones.

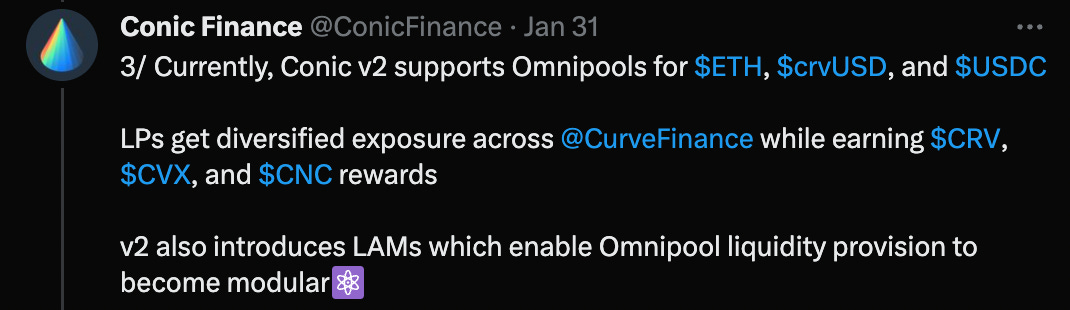

Conic V2 was launched with support for ETH, crvUSD, and USDC Omnipools, offering LP rewards in CRV, CVX, and CNC tokens. LPs can also participate in LP token bonding, exchanging their crvUSD Omnipool LP tokens for vlCNC at a discount. These bonded LP tokens are then staked to earn CRV and CVX, with rewards gradually distributed to vlCNC holders.

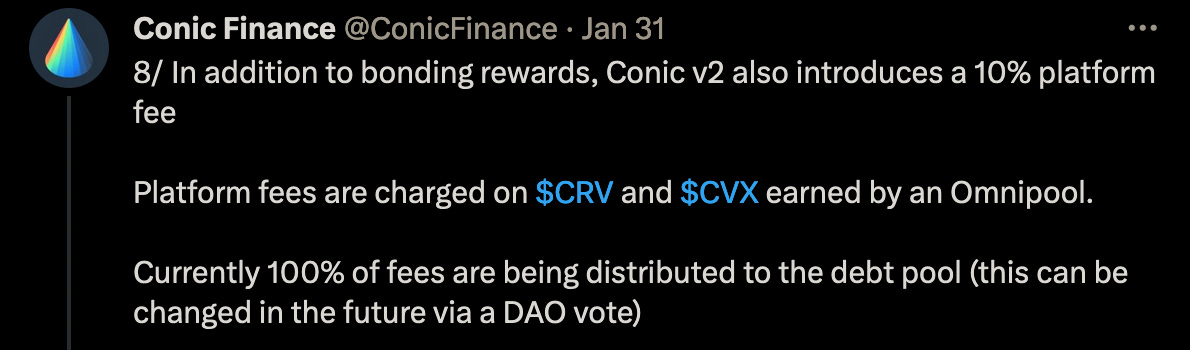

Probably the biggest change from V1 is the introduction of the 10% platform fee, which is being utilized to pay back debtors from the V1 exploit(s). Overall, it has been an exciting feature-packed launch with fantastic protocol additions.

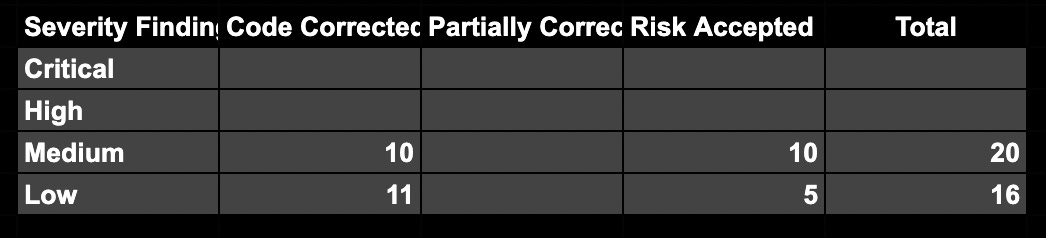

MixBytes Audit

On February 2nd, after the V2 Omnipool Launch—as per their policy—the MixBytes audit was released. The audit covered the period of September 4th, 2023, through to January 30th, 2024, with over 30 contracts audited.

The conclusion confirmed well-written smart contracts with sufficient test coverage, with 20 Medium and 16 Low-severity findings—all of which have been acknowledged and/or fixed by the Conic Team.

If you want to see the full details of each contract as part of the audit, you can find the full breakdown in the ‘Overview of Findings’ linked above.

Bonding

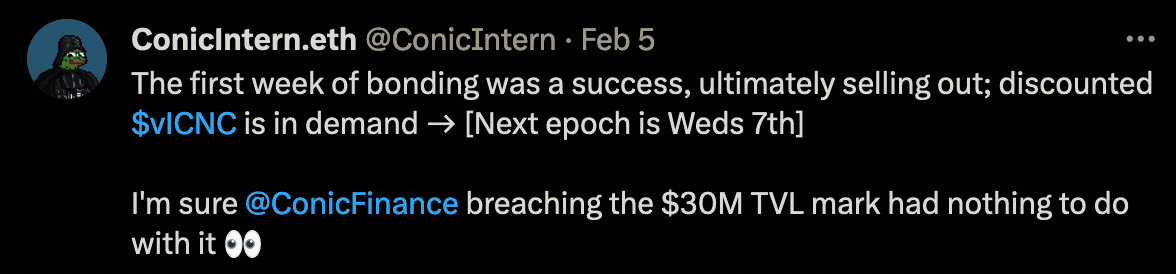

As mentioned above, the launch introduced a Bonding mechanism and was a hit amongst Coneheads, with the first Epoch being completely sold out. The cncCRVUSD LP tokens raised from the bonding program are streamed over seven days to vICNC lockers.

Initially, the vICNC APR showed some massive percents due to the need for vICNC lockers to migrate to V2’s Locker, which many hadn’t completed. However, as more Coneheads migrated for the juicy APR rewards, the figure settled at around 27.69%.

It’s worth noting that this APR is determined by the number of bonds sold in each Epoch, and as you can see above, if there is any significant volatility with CNC, the bonding amount and discount take time to adjust to offer a premium.

The team has confirmed that the bonding program will conclude after running for 52 Epochs, so keep an eye out if you’re interested in snagging discounted bonds.

Post Launch Growth

Let’s talk about growth; in less than 24 hours of launch, the protocol had surpassed $20M TVL—a significant milestone. It’s great to see support return for Conic and its Omnipool model; the team are undoubtedly grateful, and the community will be pleased.

This is just the first step; we’re still some ways from the $170M TVL all-time high, but with the introduction of LAMs, the team will be able to implement the Omnipool model into other protocols as well as Curve—the team had already given an example of Prisma.

There is still a lot of crvUSD supply that hasn’t been enticed back to Conic yet; that’s not a problem since Omnipools has only been live for a little over a week. Undoubtedly, the team will look to claw back as much as possible; we might have to wait and see how Llama Lend’s rollout impacts liquidity movement.

Another wider market consideration that stood out to us is restaking, driven predominantly by EigenLayer—which has absorbed over $5B TVL in several liquid staking tokens (LSTs) and native Ethereum on the beacon chain.

Following EigenLayer’s rise, we have seen the introduction of several Liquid Restaking Tokens (LRTs), a similar model to LSTs where individuals can deposit into these protocols and receive a liquid token for their restaked ETH.

Why is this relevant? Well, all of these protocols promise composability with future DeFi integrations, and as it currently stands, there isn’t much integration at all. We’ve seen one pool appear on Curve already, but that’s about it.

This leaves an opportunity for DeFi teams to implement integrations or help support LRT liquidity. Liquidity, you say?

Either way, with only 4% of the staked ETH supply being restaked, there is a huge growth opportunity—if, for example, Conic became the defacto liquidity destination for LRT ETH tokens and soaked up, say, 10% market share, it would be massive.

Just some food for thought, Coneheads!