05/04: The Conepaign

Napier Snapshot, Lastest LAVs, New Omnipools and Unpacking v2.1

In this latest transmission, we look at the Napier Snapshot, the Latest Liquidity Allocation Votes (LAVs) results, the FRAX and USDT Omnipools go-live, and Unpacking Conic V2.1.

The Napier Snapshot

Following up on the Napier Finance snapshot that was covered in the last Cone Link, we can confirm that it was taken as of 26th of March.

As a reminder, both vlCNC and crvUSD Omnipool LPT holders could earn the points. The airdrop target addresses holding at least 4300 vlCNC or 2 ETH equivalent portfolio values.

Latest LAV Results

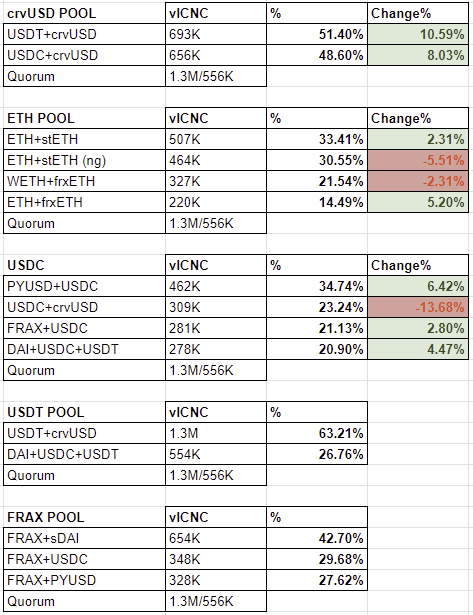

The latest LAV went live on March 28th and concluded on April 2nd. The newest distribution of each of the pools is as follows:

crvUSD POOL

USDT+crvUSD — 51.40%USDC+crvUSD — 48.60%

ETH POOL

ETH+stETH — 33.41%ETH+stETH (ng) — 30.55%WETH+frxETH — 21.54%ETH+frxETH — 14.49%

USDC POOL

PYUSD+USDC — 34.74%USDC+crvUSD — 23.24%FRAX+USDC — 21.13%DAI+USDC+USDT — 20.9%

USDT POOL

USDT+crvUSD — 66.76%DAI+USDC+USDT — 33.24%

FRAX POOL

FRAX+sDAI — 49.18%FRAX+USDC — 26.17%FRAX+PYUSD — 24.65%

The latest LAV's biggest gainers are slightly deceptive. Both crvUSD pools saw a significant redistribution following the removal of the FRAX+crvUSD pool. So, the biggest gainer was actually PYUSD+USDC in the USDC Omnipool, netting 642bps, up from 28.32% in the previous vote. In the USDC pool, USDC+crvUSD had the largest drop-down -13.68% from the previous LAV.

Per the previous removal votes, the DAI+USDC+USDT+sUSD in the USDT Omnipool and FRAX+crvUSD pool from the crvUSD Omnipool were both removed.

FRAX Omnipool goes live

On the 2nd of April, following the conclusion of the Liquidity Allocation Votes, both the FRAX & USDT Omnipools went live.

Re-introducing both Omnipools that were originally available in V1, once again further extends the Conic flywheel into the Curve ecosystem.

The protocol FX team also seems very interested in Conic, and their recent podcast with 0xPims and Robo-Odin shows this. As their protocol grows, we can definitely see them becoming a staple within the Conic Omnipool Ecosystem.

Unpacking Conic V2.1

On April 3rd, the droids dropped a new team update on the Conic governance forum.

It was quite a meaty post with several avenues that the team are now simultaneously exploring, which will tie into the next stages of the protocol. This isn’t an important step for Conic, so we want to take the time to unpack each topic and reflect on how we see it benefiting Conic.

Governance Upgrade:

Removing the complexity and challenges that arise from numerous votes, this upgrade simplifies voting, consolidates it into one to enhance efficiency, and increases the power of vlCNC.

Concentrated Directed Liquidity:

It enhances capital efficiency—and, combined with the new voting system—introduces scarcity to vICNC’s voting power. This requires holders to choose the direction of liquidity carefully.

Concentrating voting power amplifies effectiveness allowing protocols to focus their voting power on specific pools, thereby maximizing impact.

Tokenomics Upgrade:

The upgrade shifts CNC emissions to a governance-controlled model, aligning rewards with liquidity allocation. vlCNC holders will now be able to direct both liquidity and CNC emissions simultaneously.

LRT Omnipool:

Liquid Restaking Tokens (LRTs) support through the wstETH Omnipool facilitates liquidity provision for these assets.

This introduces Conic into the Restaking flywheel/narrative by enabling Liquidity Providers to farm LRT yields while allowing vlCNC holders to direct liquidity to preferred LRTs.

ETH/x Omnipool:

The ETH/x Omnipool marks Conic's transition to broader asset exposure for all assets denominated in ETH. This pool offers flexibility by allowing allocation to various Curve pools paired with ETH, enhancing diversification opportunities within the Conic ecosystem.

LOTs (Liquid Omnipool Tokens):

Offering a novel solution for Liquidity Providers: gas-efficient access to Conic yield without direct Omnipool deposits. Users can customize their yield preferences, optimizing returns while benefiting from gas savings.

This is a massive step toward improving access to Omnipool yields for smaller market participants who are interested in Conic’s fantastic yields without bearing the burden of mainnet deposits gas costs.